Fixed Annuity Examples in Pennsylvania: Guaranteed Growth Strategies

Many Pennsylvania retirees and conservative investors are looking for ways to protect their savings while earning competitive interest rates. One option that continues to attract attention is the fixed annuity.

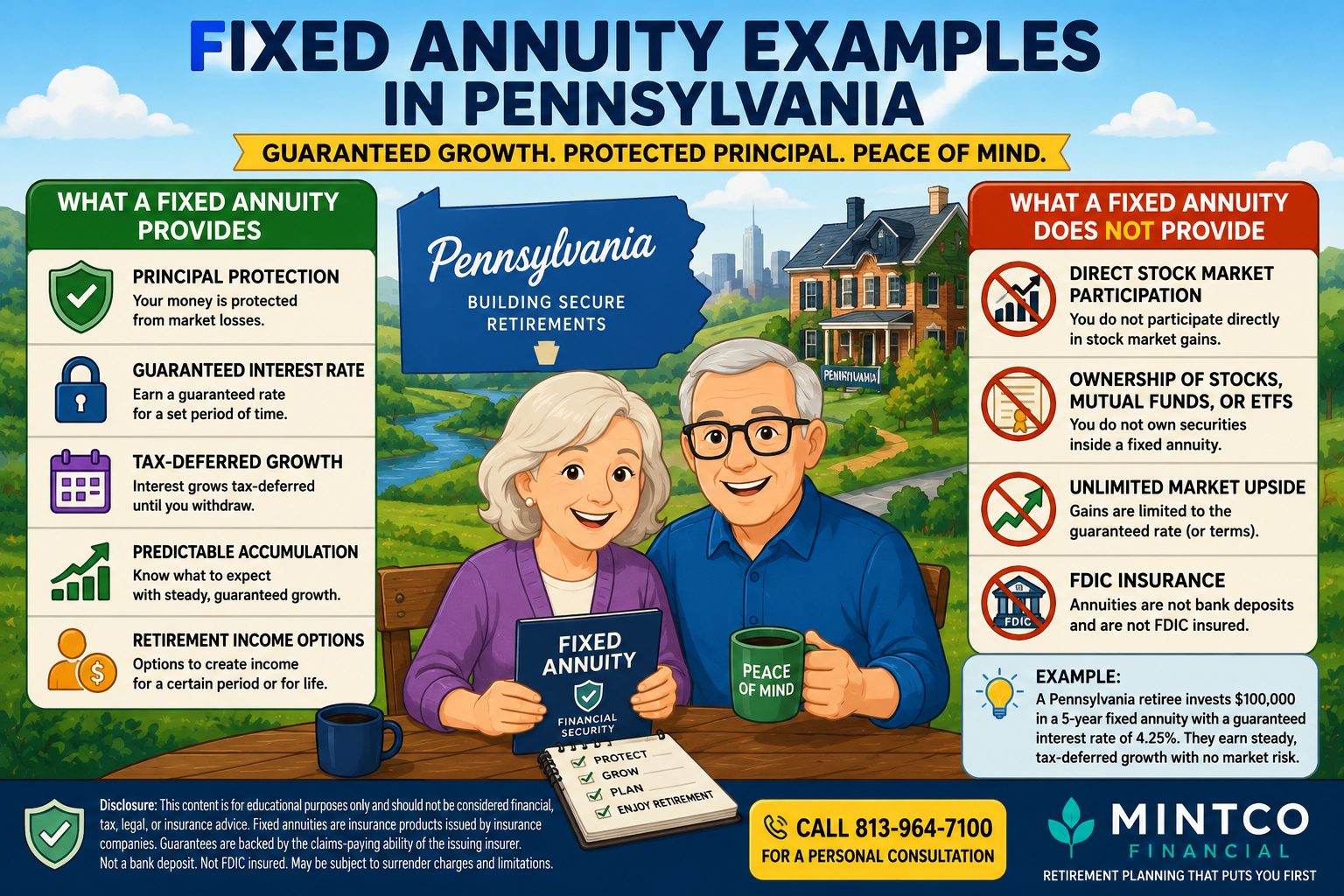

Fixed annuities are designed to provide principal protection, tax-deferred growth, and guaranteed interest rates for a specified period. They are often compared to CDs but may offer additional benefits depending on the investor’s goals.

What Is a Fixed Annuity?

A fixed annuity is a contract issued by an insurance company that guarantees a stated interest rate for a period of time. Unlike stocks and mutual funds, fixed annuities are designed to protect principal from market volatility.

Many retirees use fixed annuities to preserve retirement assets while generating predictable growth.

Fixed Annuity Example #1: Pennsylvania Retiree Seeking Safety

Mary, a 68-year-old retiree from Pittsburgh, recently sold a portion of her investment portfolio and wanted to reduce market risk.

She invested $100,000 into a fixed annuity with a guaranteed interest rate for a multi-year period.

Her goals included:

- Principal protection

- Guaranteed growth

- Tax-deferred accumulation

- Reducing stock market exposure

For Mary, the fixed annuity provided peace of mind while allowing her assets to continue growing.

Fixed Annuity Example #2: Pennsylvania CD Alternative

John and Susan from Harrisburg were comparing bank CDs with fixed annuities.

While CDs offered FDIC insurance, they were interested in tax-deferred growth and potentially higher long-term accumulation.

After reviewing their goals, they selected a Multi-Year Guaranteed Annuity (MYGA) that provided a guaranteed interest rate for several years.

Their objectives included:

- Preserving principal

- Earning a competitive guaranteed rate

- Avoiding stock market volatility

- Deferring taxes on interest growth

Fixed Annuity Example #3: IRA Rollover Strategy

A retired teacher in Philadelphia rolled over a portion of a traditional IRA into a fixed annuity.

The goal was to create a conservative portion of the retirement portfolio while maintaining tax-deferred status.

By using a fixed annuity, the investor gained:

- Guaranteed interest

- Tax-deferred growth

- Protection from market losses

- Predictable retirement planning

Benefits of Fixed Annuities in Pennsylvania

- Guaranteed principal protection

- Guaranteed interest rates

- Tax-deferred growth

- Protection from stock market downturns

- Retirement planning flexibility

- Potential alternative to CDs

What Fixed Annuities Do Not Provide

Fixed annuities generally do not provide:

- Direct stock market participation

- Ownership of stocks or mutual funds

- Unlimited market upside

- FDIC insurance

Instead, they focus on safety, guarantees, and predictable accumulation.

Frequently Asked Questions

Are fixed annuities safe?

Fixed annuities are designed to provide principal protection and guarantees backed by the claims-paying ability of the issuing insurance company.

Can a fixed annuity lose money?

Fixed annuities generally protect principal from market losses, although surrender charges, withdrawals, taxes, and contract provisions may affect value.

Are fixed annuities better than CDs?

It depends on individual goals. Fixed annuities may offer tax-deferred growth and competitive guaranteed rates, while CDs provide FDIC insurance and typically greater short-term liquidity.

Can I use IRA money?

Many fixed annuities accept qualified retirement funds, including Traditional IRAs, Roth IRAs, SEP IRAs, and rollover IRAs.

Compare Fixed Annuity Options in Pennsylvania

Learn whether a fixed annuity, MYGA, CD alternative, or retirement income strategy may fit your financial goals.

Serving Pennsylvania residents through secure virtual meetings nationwide.

Disclosure:

This material is for educational purposes only and should not be considered financial, tax, legal, or insurance advice. Fixed annuities are insurance products issued by insurance companies and are not bank deposits, not FDIC insured, and not insured by any federal government agency. Guarantees are backed by the claims-paying ability of the issuing insurance company. Product features, rates, surrender charges, and availability vary by carrier and state. Consult qualified professionals regarding your individual financial situation before making investment or insurance decisions.

“`