Fixed Indexed Annuities in California and Florida: 2026 Guide

Fixed Indexed Annuities, also known as FIAs, are often considered by retirees who want principal protection, tax-deferred growth, and the opportunity to earn interest linked to a market index without directly investing in the stock market.

For retirees in California and Florida, FIAs may be part of a broader retirement income strategy, especially for those concerned about market volatility, inflation, and running out of money in retirement.

What Is a Fixed Indexed Annuity?

A fixed indexed annuity is an insurance contract issued by an insurance company. Your interest may be linked to the performance of an index, such as the S&P 500, but your money is not directly invested in the market.

If the index performs well, you may earn interest based on the contract’s crediting method. If the index performs poorly, your contract may provide downside protection, subject to the terms of the policy.

Why Retirees Consider Fixed Indexed Annuities

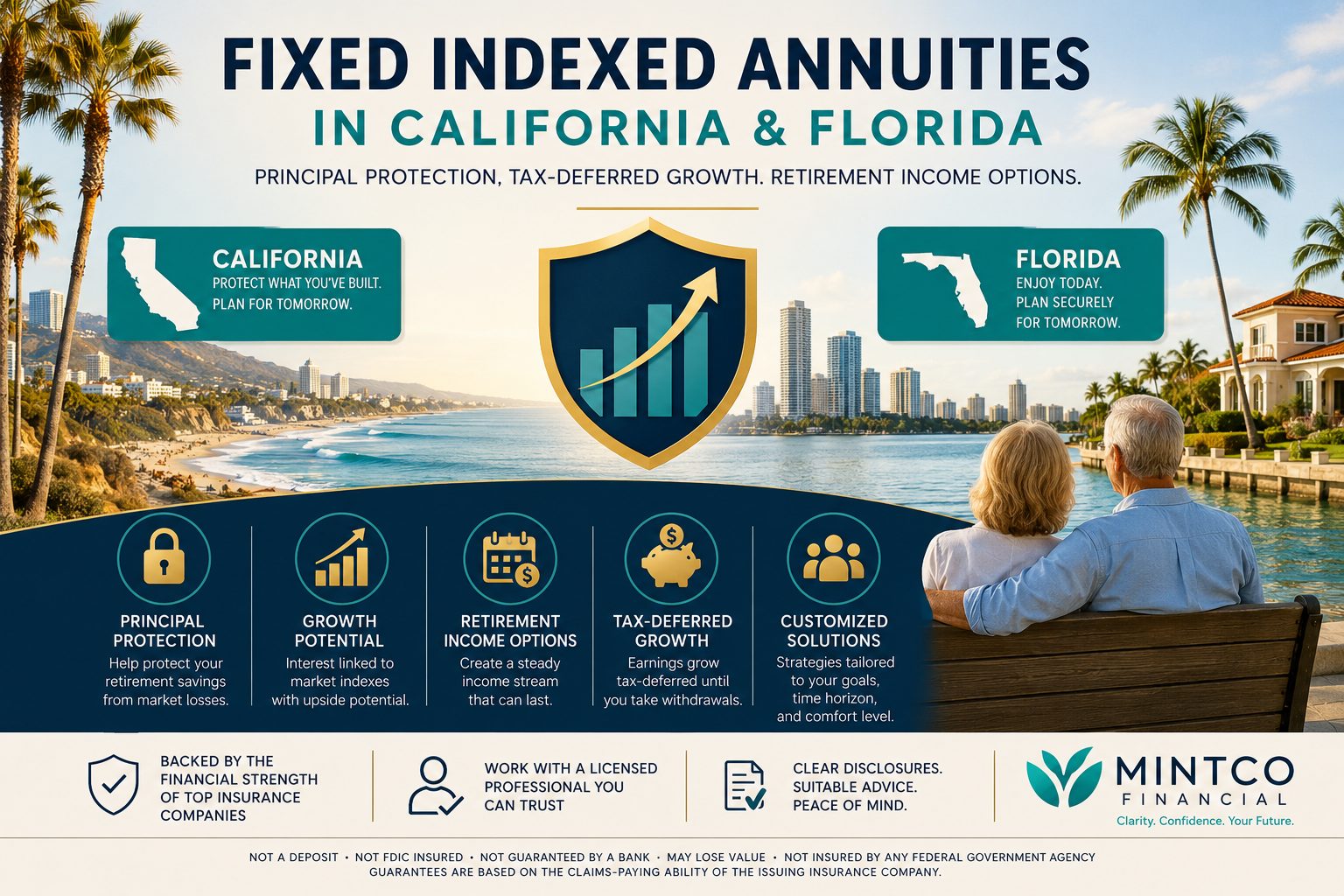

- Principal protection from market losses

- Tax-deferred growth

- Potential interest based on index performance

- Optional income riders

- Retirement income planning

- Protection against sequence-of-returns risk

Fixed Indexed Annuities in California

California retirees often face high living costs, taxes, healthcare expenses, and concerns about preserving retirement assets. Because California is also known for a highly regulated financial and legal environment, it is especially important that annuity recommendations are clearly explained, suitable, and properly documented.

Before purchasing a fixed indexed annuity in California, investors should carefully review surrender charges, income rider costs, cap rates, participation rates, spreads, withdrawal rules, and how the policy fits into their overall financial plan.

Fixed Indexed Annuities in Florida

Florida retirees often look for retirement income strategies that provide stability, tax deferral, and protection from market downturns. Since Florida has no state income tax, many retirees focus on preserving income, reducing volatility, and creating a retirement plan that can last for decades.

A fixed indexed annuity may be appropriate for some Florida retirees, but it should be compared with other options such as CDs, MYGAs, bonds, investment portfolios, and other retirement income strategies.

Are Fixed Indexed Annuities Safe?

Fixed indexed annuities are not stock market investments. They are insurance contracts backed by the financial strength and claims-paying ability of the issuing insurance company.

They may protect principal from market losses, but they are not FDIC insured, are not bank deposits, and may include surrender charges or limitations on withdrawals.

Common Questions About FIAs

Can I lose money in a fixed indexed annuity?

Fixed indexed annuities generally protect against direct market losses, but you may lose access to liquidity or incur surrender charges if you withdraw too much too early.

Are fixed indexed annuities better than CDs?

It depends on your goals. CDs may offer FDIC insurance and liquidity, while FIAs may offer tax deferral, principal protection, and potential income features.

Are FIAs good for California retirees?

They may be suitable for some California retirees, but due to the state’s regulatory and legal environment, clear documentation, suitability, and full disclosure are especially important.

Are FIAs good for Florida retirees?

They may be useful for Florida retirees who want principal protection, tax-deferred growth, and retirement income options, but they should be evaluated carefully.

Do fixed indexed annuities have fees?

Some FIAs have no annual fee unless optional riders are added. Income riders, enhanced benefits, or special features may include additional costs.

Compare Fixed Indexed Annuity Options

Not all fixed indexed annuities are the same. Rates, caps, participation rates, income features, surrender periods, and carrier ratings vary significantly.

Mintco Financial can help compare options from multiple insurance companies and explain how a fixed indexed annuity may or may not fit your retirement plan.

Compare Fixed Indexed Annuities

Explore retirement income strategies designed to help protect principal, reduce market risk, and create long-term financial confidence.

Serving clients in California, Florida, and nationwide through secure virtual meetings.

Fixed Indexed Annuities

California • Florida • Nationwide

Compare options today

Important Disclosure:

This content is for educational and informational purposes only and should not be construed as individualized financial, investment, legal, tax, or insurance advice. Fixed Indexed Annuities are insurance contracts issued by insurance companies. They are not bank deposits, are not FDIC insured, are not guaranteed by any bank, and are subject to the claims-paying ability and financial strength of the issuing insurance company.

Fixed Indexed Annuities are not direct investments in the stock market or any index. Index performance does not include dividends unless specifically stated in the contract. Interest crediting methods, caps, participation rates, spreads, surrender periods, withdrawal provisions, rider fees, and product availability vary by carrier, state, and individual circumstances.

Withdrawals before the end of the surrender period may be subject to surrender charges, market value adjustments, and taxes. Withdrawals before age 59½ may also be subject to IRS penalties. Optional riders may involve additional costs and may not be appropriate for all clients.

California and Florida clients should carefully review all contract terms, suitability requirements, disclosures, and financial objectives before purchasing an annuity. No annuity should be purchased based solely on advertised rates, income illustrations, bonuses, or guarantees without understanding the full contract terms.

Mintco Financial does not provide legal or tax advice. Please consult your CPA, tax advisor, attorney, and licensed financial professional before making any annuity or retirement planning decision.